Key takeaways:

For 2026, the health savings account (HSA) contribution limits rise to $4,400 for people with self-only coverage and $8,750 for those with family coverage, up from $4,300 and $8,550 in 2025.

You can use your HSA to pay for a variety of qualified medical expenses, including prescription medications and eyeglasses.

Starting January 1, 2026, you'll also be able to use your HSA to pay for direct primary care (DPC) membership fees if certain requirements are met.

You have until April 15 to make HSA contributions for the prior year. That means for tax year 2026, you can make HSA contributions until April 15, 2027. However, you can only contribute to your account during the months you’re considered HSA eligible.

Health savings accounts (HSAs) continue to grow in popularity. Data collected by Devenir shows that total HSA assets had reached nearly $147 billion across more than 39 million accounts as of December 31, 2024.

An HSA is a tax-advantaged savings account that allows you to set aside money to pay for qualified medical expenses. Contributions are made with pretax dollars, and the funds can grow tax-free and be withdrawn tax-free when used for eligible healthcare costs.

Before you put money into an HSA, it’s important to understand the contribution limits. While the IRS has increased the limits for 2026, your personal contribution cap will depend on several factors, such as your age, whether you have self-only or family coverage, and whether you qualify for catch-up contributions.

Search and compare options

Below, we will review the new HSA contribution limits for 2026 and explain how they vary based on coverage type and age.

What are the HSA contribution limits for 2026?

For the 2026 tax year, the IRS has increased the contribution limits for HSAs. If you have self-only high-deductible health plan (HDHP) coverage, you can contribute up to $4,400 to your HSA. If you have family HDHP coverage, the contribution limit rises to $8,750.

Catch-up contributions for people ages 55 and older

If you’re 55 or older by the end of the tax year and not enrolled in Medicare, you’re allowed to contribute an additional $1,000 to your HSA as a catch-up contribution. This means:

If you’re 55 or older and have self-only HDHP coverage, you can contribute up to $5,400 in 2026.

If you’re married and have family HDHP coverage, your standard contribution limit is $8,750 in 2026.

If both you and your spouse are age 55 or older and not enrolled in Medicare, each of you can make a $1,000 catch-up contribution to your own HSA. Your total combined family contribution limit is $10,750 in 2026.

When can you contribute to an HSA for 2026?

You can begin making HSA contributions for the 2026 tax year as early as January 1, 2026. You don’t have to contribute the full amount all at once. You have until the tax filing deadline of April 15, 2027 to reach your annual limit. However, if the IRS extends the tax filing deadline, the HSA contribution deadline will also be extended.

How do I calculate my maximum HSA contribution amount for 2026?

Your maximum HSA contribution amount for 2026 will depend on several factors, including:

The type of HDHP you are enrolled in (i.e., self-only or family)

Your age

Which months you are eligible to contribute to an HSA

Whether you qualify for the HSA last-month rule

Let’s say that, in 2026, you will:

Be 43 years old

Have self-only HDHP coverage

Be enrolled in an HDHP for only 6 months

Since you will not be HSA eligible for the entire coverage year, you’ll need to prorate your contribution limit. In this case, you can contribute up to 50% — or 6 months’ worth — of the annual limit. Instead of being able to contribute the full $4,400 to your HSA, your contributions will be capped at $2,200 for 2026.

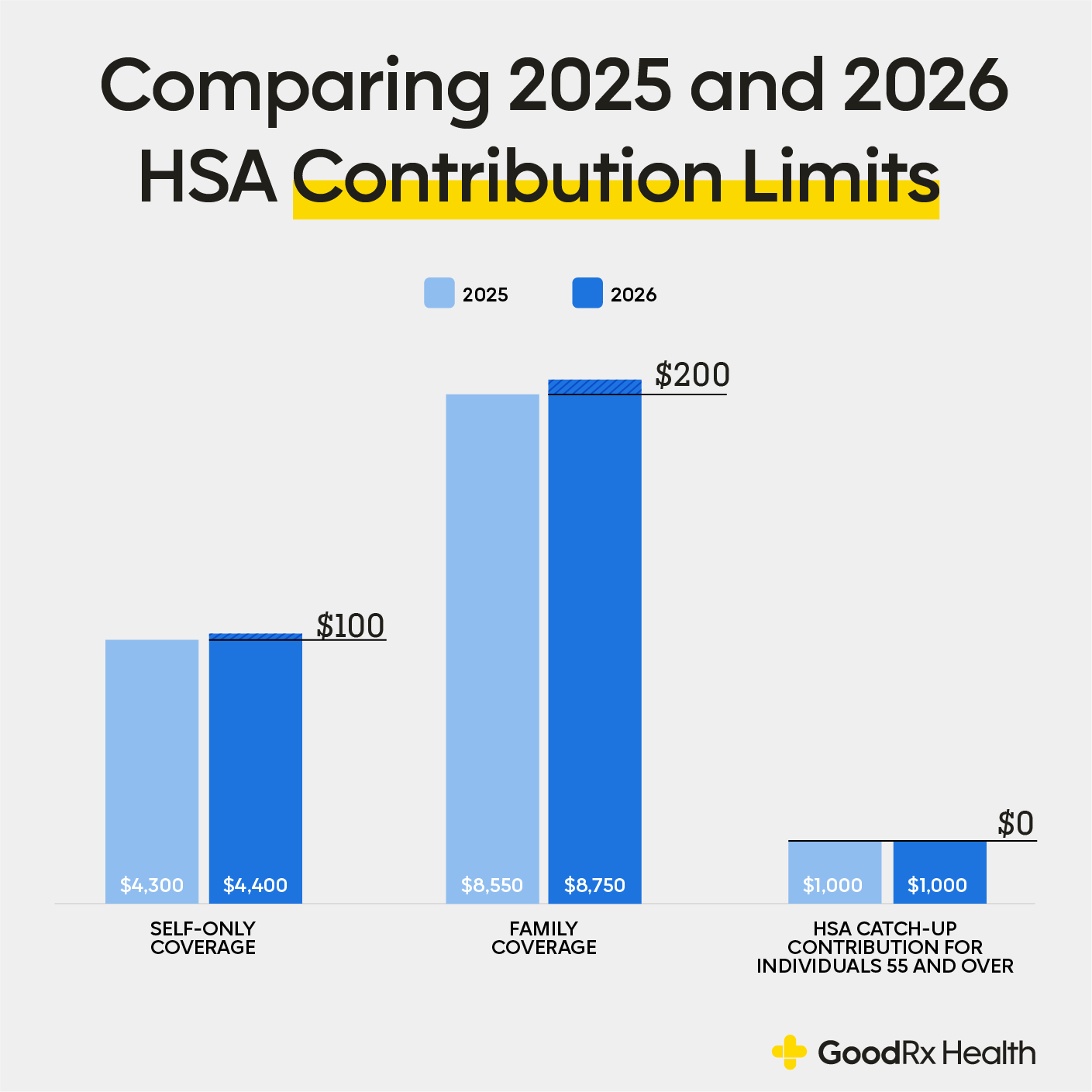

How do the HSA contribution limits for 2026 compare with the ones for 2025?

HSA contribution limits are increasing from 2025 to 2026. For 2026, the HSA contribution limit is $4,400 for people with self-only coverage, up from $4,300 in 2025. For people with family coverage, the contribution limit for 2026 is $8,750, up from $8,550 in 2025.

Below is an infographic that shows the changes in contribution limits from 2025 to 2026.

What expenses will be HSA eligible in 2026?

If you have an HSA, you will be able to use your funds to pay for a variety of qualified medical expenses tax-free in 2026. These include common healthcare costs like copayments, deductibles, prescription medications, dental work, and vision care.

You can also invest unused HSA funds and use them in the future, even during retirement. But if you want to save money on healthcare costs in 2026, here are some HSA-eligible expenses you will be about to use your funds for:

Dental care (e.g., cleanings, fillings, and dentures)

Eye exams and prescription eyeglasses and contact lenses

Hearing aids and batteries

Menstrual care products (e.g., tampons, pads, period underwear)

Over-the-counter medications

Wheelchairs and other medical equipment

You can also use your HSA to pay for prescription medications, including popular medications like:

Albuterol (Ventolin) for asthma and breathing difficulties

Amlodipine (Norvasc, Katerzia, Norliqva) for high blood pressure

Atorvastatin (Lipitor, Atorvaliq) for high cholesterol

Mounjaro (tirzepatide) for Type 2 diabetes

Wegovy (semaglutide) for chronic weight management

Starting January 1, 2026, you can use your HSA funds to pay for direct primary care (DPC) membership fees. DPC is a healthcare model where you pay your healthcare professional or clinic a flat monthly or annual fee for primary care services instead of billing insurance. Under the One Big Beautiful Bill Act, these membership fees are now considered qualified medical expenses, and DPC arrangements are no longer treated as health plans for HSA purposes. However, the monthly fee must not exceed $150 for an individual or $300 for a family plan.

What expenses will not be HSA eligible in 2026?

In general, you cannot use your HSA for:

Expenses reimbursed by your insurance plan or another source

Nonmedical expenses (unless you're over age 65, in which case withdrawals will be taxed but not penalized)

Cosmetic procedures

Will money in your HSA roll over from the previous year?

Yes, your unused HSA funds will roll over automatically from 2025 to 2026. One of the benefits of an HSA is that you don’t lose unused money at the end of the year. Any remaining balance in your HSA carries over into the next year. Unlike with a flexible spending account (FSA), there is no deadline to spend the funds in an HSA account.

The bottom line

HSA contribution limits have been increased again for 2026. For the 2026 tax year, you can contribute up to $4,400 if you have self-only coverage, compared to $4,300 in 2025. If you have family coverage, you can contribute up to $8,750, which is $200 more than the 2025 limit. Keep in mind that these are the standard contribution limits for 2026. Your personal HSA contribution limit will depend on multiple factors, including your age and which months you are HSA eligible.

Why trust our experts?

References

Devenir. (2025). Devenir report shows HSA assets reach nearly $147 billion by year-end 2024.

Internal Revenue Service. (2025). 26 CFR 601.602: Tax forms and instructions.

U.S. 119th Congress. (2025). H.R.1 - One Big Beautiful Bill Act.