What Is Medicare?

Medicare is a federal health insurance program for people ages 65 and older. Younger people with long-term disabilities, permanent kidney failure, or amyotrophic lateral sclerosis (known as ALS or Lou Gehrig’s disease) are also eligible. Enrollees can receive these healthcare benefits no matter their income, medical history, or health status.

Medicare and Medicaid were created by federal law in 1965. Benefits later expanded to cover prescription medications. Today the Centers for Medicare & Medicaid Services oversees Medicare, which covers more than 70 million people.

Medicare doesn’t provide for every need. For example, assisted living and long-term care aren’t included. But this insurance does cover many preventive, routine, and emergency medical services for older adults and younger people with disabilities.

The uninsured rate for people ages 65 and older is less than 1% But in the early 1960s it was almost 50%.

Search and compare options

The Social Security Administration determines Medicare eligibility. There are three ways to qualify for Medicare:

Being ages 65 and older while meeting citizenship and residency requirements

Having a disability at any age

Having permanent kidney failure (end-stage renal disease) or ALS at any age

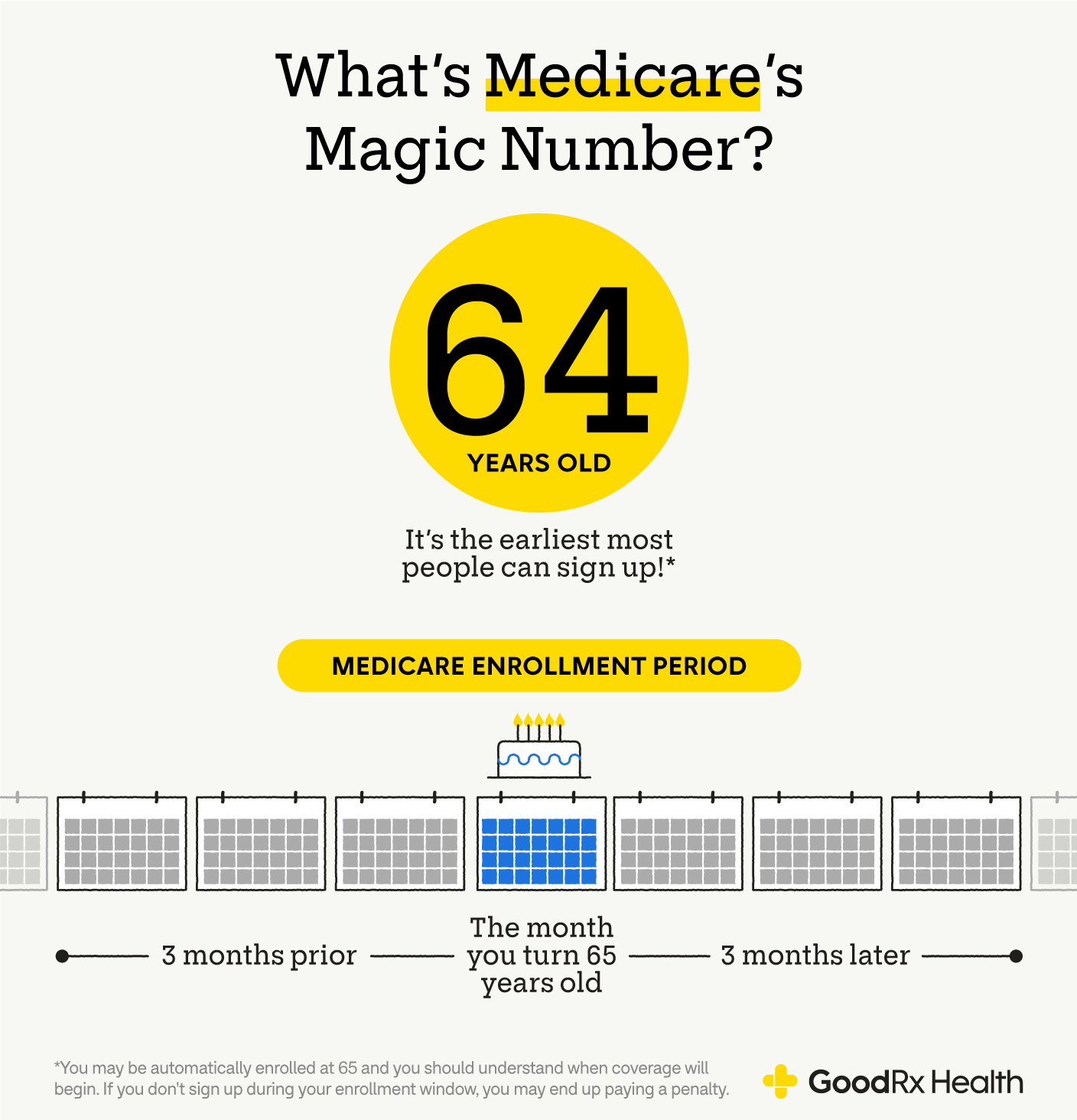

Those who qualify for Medicare based on age become eligible to apply 3 months before they turn 65. People younger than 65 who receive Social Security Disability Insurance (SSDI) typically have to wait 2 years to become eligible for Medicare. Those who receive SSDI for permanent kidney failure or ALS become eligible right away with no waiting period.

There are several ways to have Medicare coverage. For example, you can be retired and have Medicare as your primary form of coverage. Or you can keep working and make Medicare your secondary payer.

Medicare has several components that we’ll explain in more detail later. For now, here is a chart that briefly outlines the insurance plan design.

Medicare is divided into parts to cover different areas of healthcare. Medicare Part A is hospital insurance. Medicare Part B is medical insurance for care you receive in an outpatient or office setting. Parts A and B together are called original Medicare.

Medicare Part A is designed to pay for the most intensive needs, including:

Limited stays at skilled nursing facilities after hospitalizations

Some home healthcare

Most people don’t pay premiums for Part A. You pay only if you or your spouse worked and paid Medicare taxes for less than 10 years. In that case, monthly Part A premiums in 2026 are $311 (if your work credit is 30 to 39 quarters) or $565 (less than 30 quarters).

If you stay in a hospital, you have to pay part of your bill out of pocket before Medicare begins to cover your costs. The initial self-pay part is called the deductible. For 2026, the Part A deductible is $1,736.

Medicare Part A pays for up to 90 days of hospitalization during each benefit period. The first 60 days of a hospitalization are covered with no patient cost sharing. This means you pay nothing out of pocket after you meet the deductible. Starting at Day 61, there is coinsurance, which is your cost sharing. This changes at different stages of your care. At Day 91, you begin using your 60 lifetime reserve days. You can appeal Medicare payment or coverage decisions.

Also, make sure to sign up for Part A when you’re first eligible. Otherwise, you could face a late enrollment penalty.

Medicare Part B covers outpatient doctor visits and other medical care that’s not in a hospital. It also covers medications that aren’t included in other parts of Medicare. Services, medications, and vaccines typically covered under Part B include:

Injectable and infused drugs

Medical equipment such as walkers, wheelchairs, and power scooters

You have to pay a monthly premium for Part B. Most people pay the standard Part B premium, which is $202.90 in 2026. Enrollees with higher incomes pay more through a surcharge. This is called the income-related monthly adjustment amount (IRMAA). After you meet your annual deductible, you’ll pay 20% coinsurance for most services.

People with low incomes may qualify for a Medicare Savings Program (MSP). These state-offered programs help with Part B premiums. If you qualify for an MSP, you automatically get Extra Help. This reduces your out-of-pocket costs for prescription medications.

If you don’t sign up for Part B when you’re first eligible, you could face a late enrollment penalty.

Medicare Part C is known as Medicare Advantage. Under a Medicare Advantage plan, private insurance provides the same coverage as Parts A and B. In other words, Medicare Advantage is a different way of getting hospital and medical coverage included in original Medicare.

More than half of Medicare enrollees are covered by Medicare Advantage plans. These private plans bundle Part A, Part B, and often Part D. Many include routine dental care, vision benefits, hearing aids, and gym membership. By law, Medicare Advantage plans must meet or exceed original Medicare coverage.

But there are potential downsides with Medicare Advantage. These plans come with network restrictions, so you’re limited to certain doctors and hospitals in your area. Some plans let you go out of the network if you’re willing to pay higher costs. Original Medicare enrollees can go to almost any healthcare professional or hospital in the U.S.

Whether you’re turning 65 or it’s open enrollment, you may have many Medicare Advantage options. For the 2026 coverage year, enrollees can choose from, on average, 32 Medicare Advantage plans with Part D coverage and seven without Part D.

Part C costs vary based on the plan you choose. But you must pay your Part B premium even when you have Medicare Advantage. The out-of-pocket maximum for Medicare Advantage plans in 2026 is $9,250 for in-network covered services. It is $13,900 for in-network and out-of-network covered services combined.

You cannot combine Medicare Advantage with Medigap. So there’s no supplemental insurance to help with Medicare Advantage out-of-pocket costs.

Medicare Part D is prescription drug coverage. You can add it to your original Medicare plan, which doesn’t cover medications. Part D is included in most Medicare Advantage plans, but you can add this coverage if it’s not.

Part D plans are optional when you have Medicare. But if you don’t have other drug coverage when you enroll in Medicare, you could face a late enrollment penalty.

Because of the different parts, you may pay two or three Medicare premiums per month. Many people use their Social Security payments for their Parts B and D premiums.

If you don’t have creditable drug coverage that matches Medicare’s benefits, you can buy a Part D plan from a private insurance company. Premiums vary, and higher-income enrollees may pay more because the IRMAA surcharge applies to Part D. Plan deductibles can’t exceed $615 in 2026.

You can use the Medicare Plan Finder to compare Part D plans. When you’re deciding on prescription coverage:

Check each formulary to see if the medications you need are covered.

Check which pharmacies are “preferred” in your plan’s network. Using those can help lower your costs.

What you pay for medications also depends on which coverage stage you’re in. Medicare Part D has three stages:

Deductible stage

Postdeductible or initial coverage stage

Catastrophic stage, which occurs after you pay $2,100 in 2026; after that, Part D pays 100% for covered medications for the rest of the year

Medicare Part D has its own premium if you have a stand-alone prescription plan. If you have a Medicare Advantage plan, prescription coverage may be included. If not, you will need to buy a stand-alone plan to have your medications covered. Here’s a summary of Part D costs:

Deductible stage: When you begin accessing prescription medications in a plan year, you have to pay a deductible. Your deductible can’t exceed $615 in 2026. After you meet your deductible, you’re responsible only for copays and coinsurance.

Initial coverage stage: Your plan shares the cost of your covered medications. You pay only coinsurance or copays, depending on your benefits and your prescriptions.

Catastrophic stage: The Part D out-of-pocket cap in 2026 is $2,100. After that, your Medicare prescription plan pays 100% of the costs of your covered medications for the rest of the year.

The Medicare Drug Price Negotiation Program was established by the Inflation Reduction Act of 2022. The law has reduced the maximum fair price for its first round of high-cost medications covered by Medicare Part D — 10 to start — effective January 1, 2026. Price drops for more medications will be effective in 2027 and 2028 for drugs covered by Parts D and B.

If you have original Medicare, you may pay a separate premium for a supplemental insurance policy known as Medigap to cover out-of-pocket costs. Depending on the plan, your covered costs can include Parts A and B deductibles and coinsurance. In some cases, Medigap plans also cover emergency healthcare during international travel. You can’t have a Medigap plan if you’re covered by Medicare Advantage.

The Medicare GLP-1 Bridge program is a pilot project that lets Part D enrollees access certain glucagon-like peptide-1 (GLP-1) medications for weight loss with a $50 monthly copay. The Medicare GLP-1 Bridge program will run from July 1, 2026 to December 31, 2027. All formulations of the following GLP-1 medications are included: the oral tablet Foundayo (orforglipron), Wegovy (semaglutide) pills and injections, and the Zepbound (tirzepatide) KwikPens. Zepbound single-use pens and vials are not included.

Medicare has different enrollment periods, depending on eligibility. Around the time you turn 65, you have a 7-month initial enrollment period to sign up for Medicare Part A with or without Part B. This starts 3 months before you turn 65, includes your birth month, and ends 3 months after you turn 65. But if you already receive Social Security or railroad retirement benefits when you turn 65, you probably don’t need to sign up. You’ll likely be automatically enrolled in Parts A and B.

Medicare has different enrollment periods, depending on eligibility. Around the time you turn 65, you have a 7-month initial enrollment period to sign up for Medicare Part A with or without Part B. This starts 3 months before you turn 65, includes your birth month, and ends 3 months after you turn 65. But if you already receive Social Security or railroad retirement benefits when you turn 65, you probably don’t need to sign up. You’ll likely be automatically enrolled in Parts A and B.

The annual Medicare open enrollment period in the fall is when eligible enrollees can make the most changes to their coverage. This opportunity runs every year from October 15 to December 7. Changes made during this time take effect January 1 of the following year.

Medicare Advantage enrollees have another chance to make changes during Medicare Advantage open enrollment, which lasts for the first three months of the year.

People who need help enrolling in Medicare can call 1-800-633-4227 (1-800-MEDICARE). You can also visit Medicare Interactive or the State Health Insurance Assistance Program (SHIP) for guidance.

Medicare Parts A and B don’t have yearly out-of-pocket caps. Medicare Advantage plans have annual spending limits, but they can be high — up to $9,250 for in-network services and $13,900 for both in-network and out-of-network services in 2026.

You can choose supplemental insurance (Medigap) only if you have original Medicare. It’s easiest to choose Medigap when you first sign up for Medicare because medical underwriting may be required if you want to buy a plan later, which can cause you to be denied or pay more for coverage.

There are several important changes to original Medicare, Medicare Advantage, and Part D in 2026:

Part D out-of-pocket limit: Your annual spending cap on prescriptions increases from $2,000 in 2025 to $2,100 in 2026 before your plan pays 100% for covered prescriptions for the rest of the year.

Prior authorization pilot: Beginning in January 2026, a 6-year pilot program of coverage reviews for certain Medicare Part B items and services started for original Medicare enrollees who live in Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington.

Relief for Plan Finder directory errors: If you used the Medicare Plan Finder and chose a Medicare Advantage plan based on directory errors, then found that your preferred healthcare professionals and facilities are not in your network, you can be eligible for a special election period to choose a different Medicare Advantage plan.

Medicare drug price negotiation: After years of preparation, the Medicare Drug Price Negotiation program lowered prices for 10 brand-name drugs covered by Part D, effective January 1, 2026.

Medicare is a federal program that covers eligible people in the U.S. ages 65 and older as well as younger people with disabilities. Medicaid is a joint federal-state program that provides insurance for people with low incomes in all states, Washington, D.C., and five U.S. territories.

Medicare does not cover cannabis. But some Medicare enrollees gained access to hemp-derived products for medical purposes through a pilot program that began in April 2026. Hemp is a type of cannabis plant. The eligible products primarily contain CBD and little to no THC. To qualify for the Substance Access Beneficiary Engagement Incentive pilot program, Medicare enrollees must be 18 or older, be healthy enough to participate, and have a prescription from a physician or another qualified healthcare professional. Participants cannot be pregnant or breastfeeding.

Biniek, J. F., et al. (2025). Medicare beneficiaries have 32 Medicare Advantage prescription drug plans available, on average, for 2026. KFF.

Centers for Medicare & Medicaid Services. (2025). Special election period for incorrect Medicare Plan Finder Medicare Advantage (MA) provider directory information. U.S. Department of Health and Human Services.

Prescription savings

Stop paying too much for your prescriptions. Compare prices, get pharmacy coupons, and save up to 80%.Resources

About GoodRx

Health conditions

Medications & treatment

Access & affordability

Well-being

Medication discounts