Key takeaways:

When his dog’s medical emergencies delivered a blow to his finances, Brian Gregg took a deep dive into researching pet insurance.

He explored the two main types of pet insurance: comprehensive and accident-only.

After calculating the costs, Brian decided to pass on pet insurance.

In 20 years as a dog owner, I never really thought about pet insurance. That all changed in a span of 2 months in 2023.

My two rescue dogs are my second set of pups. When I first welcomed a dog into my life, it was a 6-week-old, full-blooded German shepherd whom I named Vegas. He was loyal and always by my side, even waiting outside the bathroom while I showered. That first year, it was just us. And he did, indeed, become this man’s best friend.

I met Brooke, who would eventually become my wife, a year after I took Vegas home. Brooke had a pup of her own: a full-blooded Weimaraner named Murphy. He and Vegas grew old together, eventually passing away within 7 months of each other. At 13, Vegas could not overcome a bout of degenerative myelopathy, a spinal cord condition that made his hind legs weak. And Murphy tore both of his canine cruciate ligaments — a common knee injury for dogs.

Search and compare options

We adopted Stella a month after losing Murphy. We noticed her brother on a stray animal adoption website. But, when we visited with him, his rambunctious nature was a little too much for my 5-year-old daughter and 3-year-old son. The more docile 6-week-old Stella was a perfect fit.

Three years later, when the pandemic hit, life drastically changed in our household. I started a new job the week the world shut down, working more than 60 hours a week. My wife, who teaches children with severe disabilities, was working from home and making sure our two children succeeded with remote learning. It was not uncommon for me to come home after an extra-long day to find her mentally and physically spent.

As my wife’s 40th birthday approached that November, it was clear the pandemic would crush our dreams of going on a planned Hawaiian vacation. But I still wanted to do something special to celebrate and told her to name a gift.

She saw a dog on the adoption website who had brown markings that looked like Stella’s black ones. And a week later, 8-month-old Luna joined the family, becoming one of millions of pets adopted during the pandemic. Temperament-wise, she’s the opposite of her sister: rambunctious bordering on destructive. Together, Stella and Luna — Italian for stars and moon — are the empresses of the Gregg household.

Vet bills start stacking up

In the summer of 2023, both Stella and Luna had medical emergencies. And we entered canine crisis mode.

It started when we noticed Stella trying to go to the bathroom, but not succeeding. We visited the vet to investigate.

Read more like this

Explore these related articles, suggested for readers like you.

The first vet bill, which came out to a grand total of $952, included:

An injection of cerenia, to treat vomiting

Cerenia tablets

A fecal centrifugation lab, to test for intestinal parasites

IV catheter, for fluids and medication

Bloodwork

Radiography study with dexdomitor injections, to help get clear X-rays

Ultrasonography, to detect lesions

Within a few days, Stella was back to normal.

A few weeks later, Luna got excited and wanted Stella to chase her. As she does, Luna — or Lunatic, as we sometimes call her — ran around the fenced-in backyard at cyclone speed, with Stella in slow pursuit. Seconds later, Luna limped back to us with a gaping hole in her side, likely the result of sideswiping a tree or some other landscaping.

This mishap went down on a Sunday, requiring us to visit an emergency veterinarian hospital instead of her normal vet. Like taking a car to the dealer or buying food in the airport, that meant we could expect to pay top dollar.

All in, that second vet bill cost $784 for:

Emergency consult

Laceration care

Carprofen, for canine arthritis and pain

Amoxicillin, an antibiotic

Lidocaine, a local anesthetic

Dexmedetomidine, for sedation

Methadone, for pain

Atipamezole, to reverse sedation

A few days later, we noticed that a lump on Stella’s side — one we had been watching for months — had grown bigger and harder. To take advantage of a scheduled vet visit to remove Luna’s stitches, we called and asked if the vet could also take a look at Stella’s lump.

That visit and the third vet bill ended up costing us $420, with charges for:

Stitches removal

Fine-needle aspiration, to take a biopsy

Cytology, to test for cancer

The news was not good. Stella had a stage 2 mast cell tumor that needed to be removed. So we scheduled the appointment and anxiously hoped the cancer had not spread.

The procedure earned us the fourth vet bill, which totalled $1,190 and included:

Acepromazine, for sedation

Polyflex injection, an antibiotic

IV catheter

IV fluids

Histopathology, to test tissue for disease

Surgical resection, to remove part of an organ

Anesthesia, to prevent pain

Gabapentin, for pain and anxiety

Amoxiclav, to treat infection

That’s $3,346, if you are counting at home. Throw in the Benadryl and Zyrtec we bought on our own for Stella, and you can call it an even $3,400.

Is pet insurance worth it?

So, yes, the idea of pet insurance entered my mind. I did my research, and it was a close call.

There are two main types of pet insurance: comprehensive and accident-only. Comprehensive insurance covers accidents, injuries, chronic illness, infections, hereditary diseases, diagnostic care, and emergency care. Accident-only insurance primarily covers accidents and injuries.

In my mind, if I am going to buy insurance, I’d want to cover everything, so comprehensive coverage would be my choice. But even that wouldn't mean coverage for vaccinations, annual checkups, and wellness visits. I’d have a deductible and annual maximum, and I wouldn’t be reimbursed for 100% of costs. More likely, I would be reimbursed for 60% to 90% of the costs.

The average cost of comprehensive insurance for one dog is $53 per month, or $640 a year. That’s $1,280 per year for my two dogs. If I paid that for 3 years, it would cost slightly more than the $3,400 I shelled out for the worst 2 months of their lives.

And what about after that? If they live to be 13 like Vegas, I’d likely spend at least $16,640 insuring them. They’d have to suffer a whole lot of canine calamities to make it worth it.

No doubt, there are dogs that accumulate more than $8,000 in medical expenses over their lifetime. But, minus the uncovered costs of annual checkups and wellness visits, will most dogs hit that number?

So, I wondered if accident-only coverage, at an average cost of $200 a year per dog, might be the better choice. I’d spend $5,200 over a 13-year lifetime for both dogs. And that’s much more palatable, especially when you consider costly emergency vet visits and extended hospital stays.

But, while accident-only insurance would have covered Luna’s injury, it would not have covered Stella’s more expensive treatment. And there would still be the deductibles and the fact that not 100% of costs are reimbursed. Even with pet insurance, I might still pay a great deal for treatment of an injury or disease.

A difficult final decision

That said, if your dog is accident-prone or develops cancer, the cost of comprehensive or accident-only insurance may be worth it. No one wants to be hit with thousands of dollars in unexpected vet bills. Just as with homeowner’s insurance, auto insurance, or liability insurance, you are buying peace of mind.

I’m lucky to have an option; I can afford emergencies. Because of the cost, many pet owners do not. In my research, I did discover there are financial assistance programs available. But there’s no guarantee of receiving help.

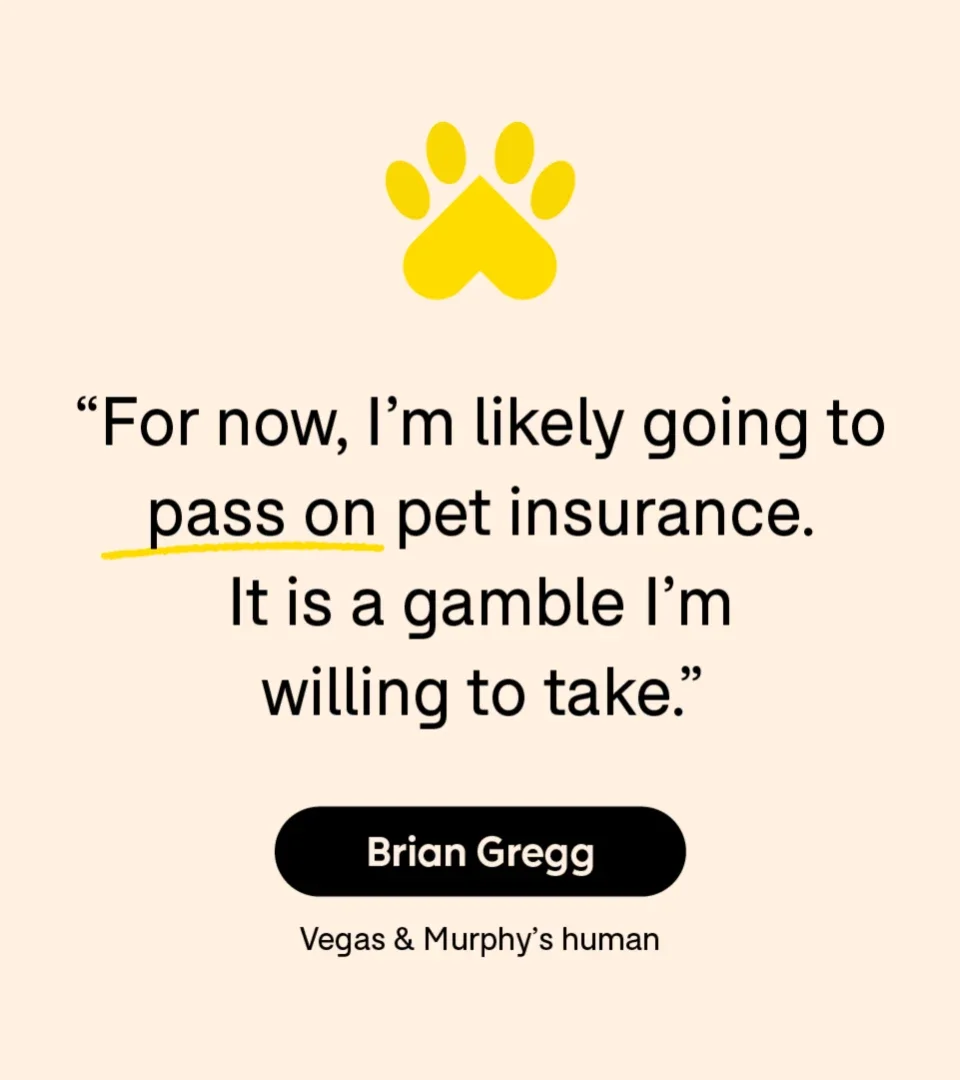

For now, I’m likely going to pass on pet insurance. It is a gamble I’m willing to take: betting on good health for Stella and Luna. If something does happen to them, we’ll find a way to cover it. You can bet on that.

Why trust our experts?